MARKET ANALYSIS | PART THREE OF THE CARIBBEAN BANKING SERIES. Banked — But by Whom?

Scotiabank is taking its Jamaican crown jewel private. The deeper question is who will own the Caribbean’s banks — and whether the region can keep itself connected to the global financial system on its own terms.

By Fletcher St. Jean, MBA — Finance & Business Strategist | Advisor

The author writes in a personal capacity. In the interest of full disclosure, he is associated with a banking group in which Scotiabank holds an interest; the views are entirely his own.

On June 12, 2026 — a couple weeks after the second installment of this series asked how long the Caribbean can count on its access to the global financial system — the Bank of Nova Scotia answered a different question, one the series had not yet put. Scotiabank, a US$1.5 trillion institution that has spent the better part of a decade selling Caribbean businesses, announced that it would acquire the 28.22 percent of Scotia Group Jamaica it does not already own, pay its minority shareholders roughly J$54 billion (about C$500 million, or some US$340 million, at roughly J$158 to the US dollar) in cash, and take the 137-year-old group private — delisting it from the Jamaica Stock Exchange. One of Canada’s largest banks is not leaving Jamaica. It is buying more of it.

The mechanics are precise. Scotiabank Caribbean Holdings Limited, which holds 71.78 percent of Scotia Group, has offered J$61.50 per share (about US$0.39) — about a 13 percent premium to the 30-day volume-weighted average price — for the 878 million shares it does not own. The transaction will proceed by a court-approved Scheme of Arrangement under Jamaica’s Companies Act: it needs a majority in number and three-quarters in value of the minority shareholders who vote, and then the sanction of the Supreme Court. An independent committee of Scotia Group’s board, advised by Ernst & Young, has recommended it; the parent expects to close in the fourth quarter of 2026. The estimated hit to Scotiabank’s core capital is about five basis points — a rounding error for a bank its size.

Set against the story this series has been telling, the move first reads as a paradox. The last installment — “Banked, But for How Long?” — traced a decade in which the international banks, RBC, Scotiabank, and most recently CIBC, steadily withdrew from the Caribbean, and asked how long the region can rely on its line to the dollar system as its correspondent relationships thin. If the Canadians are leaving, why is one paying half a billion dollars to own more of Jamaica? The answer resolves the paradox — and, more importantly, reveals that the two questions this series keeps circling, how long the region stays banked and who owns the banks, are not two questions at all. They are one.

The retreat was never indiscriminate

The withdrawal of the international banks has been read, in the headlines, as a single act of abandonment. In Scotiabank’s case it was never that. It was a portfolio decision, and the Jamaica move is its other half. Beginning in 2018, Scotiabank announced the sale of its banking operations in nine non-core Caribbean markets — Anguilla, Antigua and Barbuda, Dominica, Grenada, Guyana, St Kitts and Nevis, St Lucia, St Maarten, and St Vincent and the Grenadines — most passing to Trinidad’s Republic Financial Holdings over 2019, with local variation in a couple of cases. The bank’s own explanation was candid: rising regulatory complexity, and the cost of the technology needed to meet it, had made the smaller markets uneconomic, and it would focus where it had scale. It has since pared back elsewhere in the hemisphere, in Panama, Costa Rica, and Colombia.

But concentration is not the same as departure, and the distinction matters. Where Royal Bank of Canada exited the Eastern Caribbean and CIBC has handed its entire Caribbean franchise to Bermuda’s Butterfield for US$1.8 billion, Scotiabank repositioned: it kept, and continues to invest in, its larger markets — Jamaica and Trinidad and Tobago among them, alongside the Dominican Republic — while shedding the sub-scale ones. The Jamaica transaction is the clearest expression of that strategy. This is not a bank leaving the region; it is a bank deciding, with some precision, where in the region it intends to stay and grow.

Jamaica is the clearest case of what Scotiabank chose to keep. Scotiabank has operated there since 1889. Scotia Group is the second-most-profitable bank in the country and among its five most profitable companies of any kind; it earned net profit of nearly J$20 billion (about US$126 million) in its 2025 financial year, on a return on equity of roughly 15 percent, and it is Jamaica’s largest mortgage lender, with some J$118 billion (about US$750 million) in residential loans and J$774 billion (roughly US$4.9 billion) in total assets. This is not a business an owner trims. It is a crown jewel — and the logic of taking it private is the logic of a company that has decided which assets it intends to keep, and wants all of each one.

A disclosure, and why it matters here

Let me disclose a vantage point, because it shapes how I read this. I have watched this consolidation from inside it, and earlier than most. In 2016, at Bank of Nevis International, I put a proposal to the board of the parent, Bank of Nevis Limited, to acquire RBTT’s Nevis operations as the international banks began to signal their retreat; the talks opened but did not conclude. The wave arrived in force five years later — in 2021 a consortium of indigenous banks, Bank of Nevis among them, acquired Royal Bank of Canada’s Eastern Caribbean operations, and Bank of Nevis took over the very RBTT franchise I had flagged. When I joined 1st National Bank St Lucia as Managing Director in May 2022, I led the bank through the completion and migration of its acquisition of Royal Bank of Canada’s St Lucia operations and RBTT’s in St Vincent and the Grenadines — closing the final phase that August. I note this not to claim foresight as a virtue, but because it informs what follows: I have done the buying-side work of this trend, and the question it always turns on is not only why an international bank is leaving, but who is positioned to step in — and on what terms.

The capital logic of owning all of it

Why pay to buy what you already control? A 71.78 percent owner already consolidates Scotia Group’s results, directs its strategy, and appoints its board. What it does not have is the last 28 percent of the economics — and, in a business this profitable, that is the point. Scotia Group’s minority shareholders are entitled to roughly 28 percent of its earnings, which on the 2025 result is about J$5.6 billion (some US$35 million) a year, and to the dividends that flow from them, on the order of J$1.6 billion (about US$10 million) annually. By taking the group private, Scotiabank captures the whole of that profit stream in perpetuity for a one-time payment of about J$54 billion (roughly US$340 million). On the 2025 numbers, that is a price of roughly 9.6 times the minority’s share of earnings and about 1.27 times its share of book value — a full but defensible price for a franchise compounding at a fifteen percent return on equity, and one an independent committee, advised by Ernst & Young, judged fair.

It is worth being clear about the return, because the headline cost can obscure how rational the deployment is. The cheque is large in Jamaican terms but immaterial to the parent: it costs Scotiabank roughly five basis points of core capital, a fraction of one percent of a US$1.5-trillion balance sheet. What it buys is the minority’s share of a growing, high-return earnings stream — about J$5.6 billion (some US$35 million) a year on the 2025 result, an initial return of roughly ten percent on the purchase price. On that captured profit, Scotiabank recovers its outlay in under a decade; and because the underlying earnings are compounding — group profit rose about a fifth in the most recent quarter — the effective payback is shorter still, with everything beyond it accruing to the parent in perpetuity. One caution worth stating plainly: the payback is properly measured against the minority’s roughly 28 percent slice of profit, not Scotia Group’s full earnings, since the parent already owned the other 72 percent. Measured correctly, this is not an extravagance but an accretive purchase of a quality asset at a sensible price.

Scotiabank has framed the transaction plainly: a step to optimize capital and operational efficiency across its footprint, with no material change to the Jamaican operation, and an expression of confidence in a market it has banked since 1889. The region has seen the form before — Scotiabank took its own Jamaican investment arm, Scotia Investments Jamaica, private in 2016 — and the structure is a familiar one; its other listed Caribbean bank, in Trinidad and Tobago, remains public. Those are the facts of the matter. What they portend for the wider region is the more consequential question — and it is not, in the end, about Scotiabank at all.

The public-market dimension

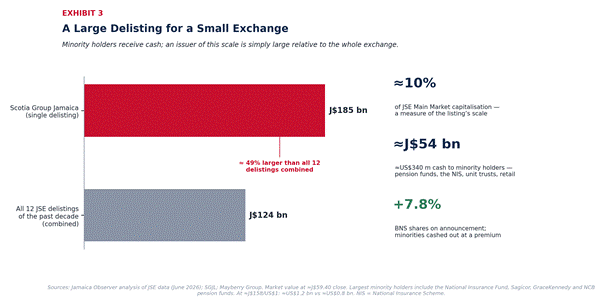

A take-private has two sides for the public market, and both deserve a fair hearing. In the immediate term it is a liquidity event of real magnitude: roughly J$54 billion (about US$340 million) in cash flows to the minority holders — pension funds, the National Insurance Fund, unit trusts, and thousands of individual Jamaicans — capital returned to investors to redeploy. As Mayberry Group’s chief executive, Gary Peart, observed, in the short term the cash coming to market is welcome. The longer-term question market participants raise is the one common to any large delisting: those investors exit a high-quality, income-producing holding, and the task — in his framing — is less finding somewhere to park the proceeds than finding a comparable holding to replace it. That is a feature of market depth, not of this transaction in particular.

The scale is a function of the company’s size. Scotia Group is worth around J$185 billion (about US$1.2 billion) at recent prices — roughly a tenth of the entire Main Market capitalization of the Jamaica Stock Exchange — so any move into private ownership is, mechanically, a large one for the exchange. For perspective, the twelve companies that delisted over the past decade had a combined pre-exit market value of about J$124 billion (some US$785 million); a single issuer of Scotia Group’s scale is larger than all of them together. The exchange has added new names over the same period, and will add more. But the structural point a Jamaican market participant framed precisely is worth noting: the question is less whether another stock can replace the listing than whether its role in a portfolio — its scale, its income, its stability — can be replicated. For institutions that depend on blue-chip income, that is the reinvestment question, and it is one about the depth of the market itself, not about any single owner’s decision.

There is a monetary footnote, offered as observation rather than concern: minority holders may elect to be paid in US dollars, converted at the Bank of Jamaica’s published rate three days before settlement. But the more interesting thread runs past this transaction to a broader one. A single take-private, fairly priced and fairly approved, is unremarkable on its own; what makes it worth a series is the pattern it sits within — the decade-long reshaping of who owns the region’s banks — and the question that pattern raises, which the last installment of this series left open.

“For how long” meets “by whom”

Return to that question. The Caribbean’s deepest banking vulnerability is not the loss of any one retail bank; it is the slow erosion of its correspondent banking relationships — the accounts that international banks hold for local ones, through which dollars clear, trade settles, and remittances move. Over the past decade the region has lost a large share of those relationships, as global banks, weighing the cost of compliance against the thin returns of small markets, simply withdrew. That is the “de-risking” this series examined: the question of for how long the Caribbean can count on its line to the world’s financial system.

The ownership story is the same story, seen from the other end. The international banks now reshaping their Caribbean footprint are not ordinary companies; they are themselves correspondent banks, or the bridges to them. A globally regulated institution like Scotiabank does not merely run branches in Jamaica; it connects them, through its own balance sheet and its network in Toronto and New York, to the dollar-clearing system. When such a bank exits a market — as Scotiabank did across the Eastern Caribbean, as RBC did, as CIBC has now done — the successor inherits the customers but not, automatically, the correspondent network. The indigenous and regional banks that step in must secure their own lines to the world, on their own balance sheets, under their own compliance regimes. Ownership, in other words, is not separate from access. It determines it: who owns a bank determines who answers for its compliance, who vouches for it to a correspondent abroad, and therefore whether it stays connected at all.

And Jamaica? Here the lesson runs the other way, and it is worth stating plainly. Scotiabank’s decision to stay and deepen is, for correspondent access, a genuine source of strength: a US$1.5 trillion parent, regulated in Canada, brings a global compliance apparatus and a ready bridge to the dollar system that few institutions in the region can match. As with any wholly owned subsidiary, that bridge runs through the parent — a general feature of group banking rather than a feature of this transaction — and the access it provides is real and substantial. It is precisely because international ownership can carry this benefit that the broader, decade-long withdrawal from other markets is what merits the region’s attention — which raises the question of what the Caribbean must build for itself where the internationals are no longer there to provide it.

What the international banks carry with them

What the international banks carry out, when they go, is not only capital and a brand. It is a compliance framework. A global bank operating in the Caribbean imports the anti-money-laundering and counter-terrorist-financing standards of its home regulator — the systems, the training, the transaction monitoring, the correspondent due-diligence discipline, and the implicit assurance, to a bank in New York or London, that an institution supervised to Canadian or American standards stands behind the local account. That assurance is itself a form of access. It is part of what has kept the region’s larger banks connected to the world.

When ownership passes to indigenous and regional hands, the customers and the branches transfer cleanly; the compliance apparatus does not. It must be built, funded, and — hardest of all — made credible to the outside institutions whose comfort determines whether the correspondent line stays open. This is the quiet, consequential work beneath the ownership headlines. A bank can be bought in a quarter; an AML/CFT framework that a foreign correspondent will trust is the work of years. The region’s banks are capable of that work — but it is work, and it is the precondition for everything else. Here ownership, compliance, and access converge into a single problem: the Caribbean cannot own its banks, and keep them banked, without owning its compliance standard too.

The compliance dividend: what the signs mean

It helps to make the connection concrete, and to do so by asking the questions a correspondent bank’s risk committee — and the regulators behind it — actually ask. Jamaica offers the clearest case study in the region, because it has just lived through the full cycle.

What does a strong AML framework actually buy a Caribbean country? Access. In February 2020 the Financial Action Task Force placed Jamaica on its “grey list” of jurisdictions with strategic AML/CFT deficiencies — a designation that tells every correspondent bank in the world to apply enhanced scrutiny, and quietly raises the cost of banking the country. Over four years Jamaica did the painstaking work: it moved from 17 of the FATF’s 40 recommendations met in 2017 to 37 by early 2024, and in June 2024 the FATF removed it from the list. The Bank of Jamaica named the payoff exactly — that exiting the grey list signals correspondent partners the country no longer requires enhanced review of its transactions. That is the compliance dividend, stated by the central bank itself: a stronger framework buys cheaper, surer access to the global system.

What does the ownership shift signal to the standard-setters — the FATF and its Caribbean arm, CFATF? That the region’s compliance capacity must not leave with the banks that brought it. As the internationals withdraw from market after market, the burden of maintaining a world-class framework falls on regional shoulders — and whether those shoulders are strong enough is precisely what the FATF’s fifth round of mutual evaluations, beginning across 2025 and 2026, will measure. There is reason for confidence: Jamaica not only exited the grey list but assumed the chair of CFATF in December 2024, and is today the only country fully compliant with the FATF’s beneficial-ownership standards. The region has shown it can clear the bar. The point is that, as ownership localizes, clearing it is no longer imported — it is the region’s own responsibility, and its own leverage.

And what does it signal to the United States — to FinCEN, the Treasury body that administers anti-money-laundering law, to the regulators who supervise the correspondent banks, and to those banks themselves? It tells them what kind of risk the region is. A correspondent bank’s decision to stay or go is, at bottom, a risk-and-cost calculation: the expected cost of compliance and potential enforcement, set against the thin revenue of a small market. A jurisdiction that strengthens its framework lowers the perceived risk and the cost-to-serve, and makes itself worth banking; a jurisdiction that lets its compliance capacity erode — as it might, if ownership localizes faster than capability is built — invites precisely the de-risking the region has spent a decade fighting. The signal the Caribbean wants to send Washington is not that it is foreign-owned or locally owned, but that it is well-governed. Ownership is the region’s to decide. The standard is the region’s to keep.

Cayman’s parallel: the safe haven that chose the rules

Jamaica is not the only proof, and the lesson is not confined to retail banking. Consider the Cayman Islands — the hemisphere’s premier offshore financial center, long shorthand for the very idea of a “safe haven.” In February 2021 the FATF placed Cayman, too, on its grey list. Over the following two years the territory did what Jamaica did: it rebuilt. It enacted a Beneficial Ownership Transparency Act, overhauled its anti-money-laundering legislation and its know-your-customer regime, empowered its financial-intelligence unit, and — crucially — began imposing real, dissuasive penalties and prosecuting money-laundering cases. In October 2023 the FATF removed it from the list; the United Kingdom and the European Union followed. A recent analysis by the corporate-services firm Ocorian captures where that left the jurisdiction: its standing as a leading funds domicile remains strong despite — and partly because of — the heavier transparency requirements, having adapted to evolving global standards while preserving the structural advantages that draw institutional capital.

That is the same compliance dividend Jamaica earned, in a different register. Where Jamaica’s prize was the renewed confidence of correspondent banks, Cayman’s was the confidence of the United States institutional investors and fund managers who route capital through it into American private markets — a role that depends entirely on its being seen, in New York and London, as clean. And it points to the force beneath this entire series. The post-2015 tightening of global standards — beneficial ownership, automatic tax reporting, sanctions enforcement, the FATF’s fourth-round evaluations — is a single pressure with two faces. It is what compelled Cayman and Jamaica to reform; and it is, in no small part, what raised the cost of compliance to the point where the international banks judged many of the smaller Caribbean markets no longer worth the candle. Reform and retreat are not separate stories. They are two responses to one demand: meet the world’s standard, or lose access to the world’s money.

The sovereignty question, globalized

Underneath all of it is a question of financial sovereignty — and no one has put that question to the world more forcefully than Barbados’s Prime Minister, Mia Mottley. In 2022 she became the first sitting head of government in nearly four decades to testify before the United States Congress, at a House Financial Services Committee hearing titled, fittingly for this series, “When Banks Leave.” Through her Bridgetown Initiative she has since carried the Caribbean’s argument into the heart of the global financial system: that an architecture designed elsewhere leaves small states paying more — to borrow, to insure, to bank — through no fault of their own, with wealthy nations borrowing at a few percent while the vulnerable pay multiples of that. It is among the most effective pieces of economic diplomacy the region has produced in a generation. The regional pattern of which this transaction is one part — the steady shift in who owns the Caribbean’s banks — is the domestic face of the same question she has globalized. If the region’s case abroad is that it must not be a price-taker in a system it did not design, then the case at home is that it must, over time, own more of the machinery of its own finance.

What the central banks see

None of this is a criticism of the regulators, whose task here is narrower and whose judgment is sound. The Bank of Jamaica has signaled no concern about the transaction, and that is the appropriate posture: the bank remains licensed, well-capitalized, locally led, and operationally unchanged; a change in the share register above it is not, in itself, a prudential event. The same central bank, it is worth recalling, is the one whose patient AML/CFT work returned the country to good standing with correspondent partners — a reminder that the prudential and the compliance mandates are, in the end, the same mandate: to keep the country bankable. The questions this transaction raises are not, in the main, for the supervisor. They are for the region’s development strategists.

Listen to those strategists and one word recurs. Jamaica sits outside the Eastern Caribbean Currency Union — it has its own central bank and its own dollar — so its banking arrangements are not the ECCB’s to manage. But the theme is regional, and the Eastern Caribbean Central Bank’s governor, Timothy Antoine, has named it more clearly than anyone. He casts his “Big Push” for the currency union not only in terms of growth but of sovereignty, and insists the region must move as one strategy, not seven silos. The Caribbean Development Bank frames the stakes in numbers: its president, Daniel Best, calls this a “decade of decision” and warns that the decade ahead cannot be financed or governed at yesterday’s scale, estimating that the region needs on the order of US$65 billion between 2024 and 2033 simply to avoid stagnation. Hold that figure beside the regional pattern and the contrast is instructive: at the very moment the region strains to mobilize capital at a scale it has never reached, the depth of its public markets and the question of who owns its largest financial assets are very much live. Mobilizing capital and retaining the capacity to own productive assets are two different problems, and the region must solve both.

The Eastern Caribbean’s particular stake

Nowhere is this question sharper than in the Eastern Caribbean Currency Union. Of the nine markets Scotiabank exited, seven are ECCU members; Royal Bank of Canada’s Eastern Caribbean withdrawal fell there too. The currency union has absorbed the heaviest concentration of the international banks’ retreat — and it is there that the questions this series has traced now press hardest. The indigenous banks and regional consortiums that stepped in hold the field; but they must now hold it together with the correspondent relationships, the compliance frameworks, and the scale that the departing internationals once supplied. The ownership is theirs. The capacity is the task.

What, then, does this mean for the ECCU going forward — and how should the region answer the call? The question belongs first to the Eastern Caribbean Central Bank, whose governor has already framed the ambition: a currency union that treats its monetary sovereignty as something to be built rather than assumed, and that meets the world as one. The response that follows is offered in exactly that spirit — not as instruction to an institution that knows its own terrain better than any commentator could, but as a contribution to the work it leads, and from someone who has done that work from inside the region’s banks: closing and migrating the acquisitions that redrew the Eastern Caribbean’s banking map, and helping build the compliance frameworks that keep institutions banked. To the ECCB and its partners, it is offered not only as analysis, but as an open hand.

From access to ownership: the work ahead

Step back, and a map comes into focus — and with it, a program of work. The international banks are not simply leaving the Caribbean; they are sorting it: the sub-scale markets sold to Republic, to Butterfield, to indigenous consortiums; the crown jewels kept and, where possible, fully absorbed. Three successor models are emerging — regional champions, offshore consolidators, and indigenous banks — and which of them comes to define Caribbean banking will be settled over the coming decade. The region is not a spectator to that settlement. It can shape it. The last installment of this series set out how; the Scotia decision makes the case more urgent. Three lines of work stand out.

First, build what the region has lacked: a correspondent of its own. The single most direct answer to a thinning correspondent panel — and to the loss of the bridge the internationals provided — is a Caribbean-owned institution, chartered with a presence and clearing access in the United States, mandated to serve ECCU and CARICOM banks as a shared correspondent. Rather than each small bank negotiating alone for a line to the dollar system, the region would pool its volume, its compliance investment, and its bargaining power into one institution built, to the highest standard, to clear dollars for its members. It is a substantial undertaking — capital, U.S. regulatory approval, and a compliance program beyond reproach are prerequisites — but it converts the region’s deepest vulnerability into a shared asset, and it is precisely the capability the departing internationals are vacating.

Second, bank as one. Governor Antoine’s insistence that the Eastern Caribbean act as one strategy, not seven silos, applies with greater force to CARICOM as a whole. A region of small, separately supervised banking systems presents the outside world with a dozen small counterparties, each individually easy to de-risk; a coordinated bloc — pooling correspondent relationships, harmonizing AML/CFT supervision, and building shared settlement — presents a single, larger, better-governed counterpart that is far harder to abandon. A unified ECCU, and a wider CARICOM that banks together, is not only a growth agenda. It is a defensive one: there is strength, and bankability, in scale.

Third, treat the compliance standard as the strategic asset it is. The lesson of Jamaica’s turnaround — and of Cayman’s — is that a strong AML/CFT framework is not a regulatory burden to be minimized but an instrument of access to be invested in — the thing that keeps the correspondent line open and foreign capital comfortable. As ownership localizes, the region must localize the compliance capability the internationals brought: shared supervisory capacity, regional training, pooled monitoring infrastructure, and a collective posture before the FATF and CFATF that converts hard-won credibility into durable leverage. Jamaica’s chairmanship of CFATF is a foundation. The work is to build a regional compliance capability that no single bank’s departure can carry away.

Beneath all three sits the need for deeper regional capital markets — exchanges able to hold and price assets like Scotia Group, and pools of local capital large enough to take meaningful stakes — which would let the region own more of what the internationals relinquish, rather than watch it pass to the next foreign balance sheet. None of this is quick. All of it is a choice.

The choice the region still holds

None of this is an argument against Scotiabank, which is entitled to optimize its portfolio, or against a fair price fairly offered to consenting shareholders and judged fair by an independent committee. It is an argument that the region should read this transaction for what it is: not an isolated piece of corporate housekeeping, but a data point in the redrawing of who owns Caribbean banking — and an invitation to decide whether that map is drawn for the region or by it. The cash will clear in the fourth quarter. The harder questions — who owns the banks, who keeps them banked, and whether the region builds the correspondent capacity, the compliance standard, and the market depth to answer both on its own terms — will take far longer, and they belong to Jamaica’s institutions, the regional central and development banks, and the wider Caribbean financial community, to whom this commentary is offered as a contribution to the work they lead.

The Caribbean Banking Series will continue. Having asked what the region’s banking access costs, how long it can be relied upon, and now who owns the banks themselves, the next installment turns to the architecture that could bind the answers together: a single, integrated Caribbean financial market — in payments, in settlement, and in capital — capable of keeping more of the region’s finance, and the decisions that govern it, in the region’s own hands.

About the author

Fletcher St. Jean, MBA, is a Caribbean financial services leader and strategist with over two decades in the sector, including service as Managing Director of 1st National Bank St Lucia Limited — where he led the completion and migration of the bank’s acquisition of Royal Bank of Canada and RBTT operations — and served as President of the Bankers Association of St Lucia. His in-depth experience spans financial-crime compliance frameworks and business and banking strategic roadmaps, and he advises on financial strategy across the region through St. Jean & Company. He writes on Caribbean finance through The Caribbean Ledger.

THE CARIBBEAN LEDGER — Independent analysis of Caribbean finance, banking, and economic strategy. Launching November 2026.

Leave a comment

You must be logged in to post a comment.